Data tokens on this page

Resources

Industry Specific

Access all the commercial banking resources your business needs to succeed.

Weekly Wealth Wire

Weekly Wealth Wire

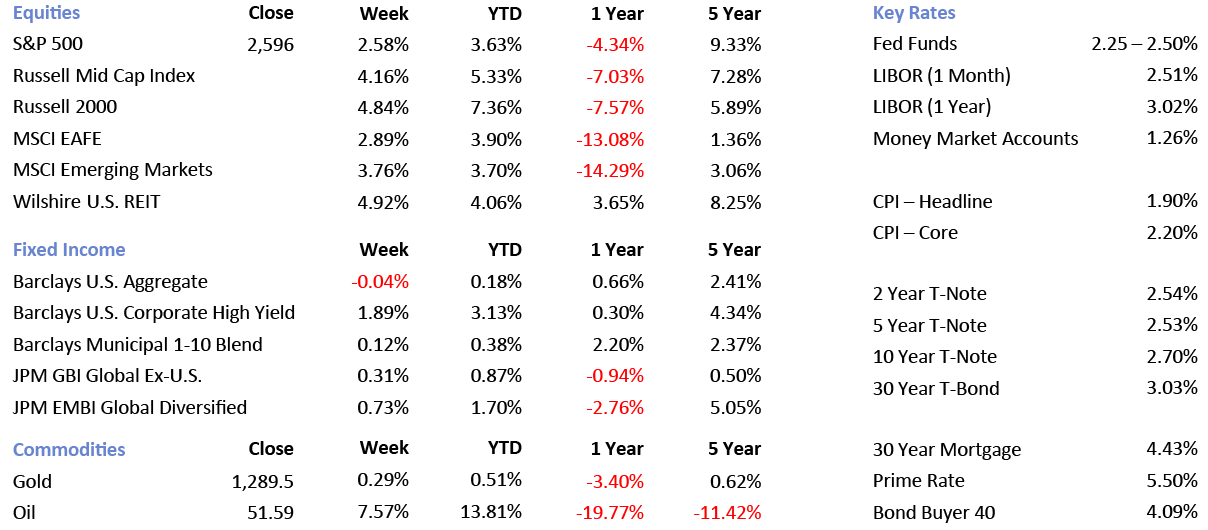

January 14, 2019 — The S&P 500 was up 2.6% last week, while the VIX index (a popular volatility measure) fell to ~18.2 for first time since early December on the strength of positive economic news. Specifically, the ISM non-manufacturing index reading registered a decline to 57.6 in December which was below expectations but still signaling expansion. The Consumer Price Index was down 0.1% in December as energy prices fell 3.5% for the month, however "core" CPI, which excludes food and energy, increased 0.2%. News regarding U.S. and Chinese trade relations was positive as well last week after the first high-level trade talks since the G20 summit last November were held. The recent talks went so well they spilled into a third day and a joint statement on progress is expected this week.

Finally, the Federal Reserve Board and the FOMC released minutes from their December meeting with several officials indicating that given "muted inflation pressures" the committee could "afford to be patient" on future rate hikes. The continued dovish comments have been well received by equity markets as the systemic rate raises of the last few years have given way to more dynamic rate decisions. In discussing financial markets for the intervening period, they noted increased volatility in asset prices from reduced risk taking by investors. They cited China and United States trade, global growth outlook, and Brexit negotiations as reasons for reduced risk taking. In review of the U.S. economy they indicated that labor market conditions continue to strengthen, industrial production continues to expand, household spending continues to increase, but real residential investment declined further in the fourth quarter. Notably, the committee concluded that "the increased concerns about global growth, made the appropriate extent and timing of the future policy firming less clear than earlier."

The Week Ahead

Key Economic Reports

- December PPI

expected: -0.1%; prior: 0.1%

- December Core PPI

expected: 0.2%; prior: 0.3%

- December Capacity Utilization

expected: 78.5%; prior: 78.5%

- December Industrial Production

expected: 0.2%; prior: 0.6%

- January Empire State Manufacturing

expected: 12.2; prior: 10.9

- January Philadelphia Fed

expected: 10.5; prior: 9.4

- January U of M Sentiment - prelim

expected: 96.0; prior: 98.3

VITAL SIGNS

Sources: briefing.com, Yahoo Finance, Kitco.com, U.S. EIA, First Trust, Wintrust Wealth Management analysis. Returns are total returns calculated through 1/11/2019 and 5 year returns are annualized. Gold is the New York spot price in $/oz. Oil is the Cushing, OK WTI spot price FOB in $/BBL. Securities, insurance products, financial planning, and investment management services are offered through Wintrust Investments, LLC (Member FINRA/SIPC), founded in 1931. Trust and asset management services offered by The Chicago Trust Company, N.A. and Great Lakes Advisors, LLC, respectively. ©2019 Wintrust Wealth Management

Investment products such as stocks, bonds, and mutual funds are:

NOT FDIC INSURED | NOT BANK GUARANTEED | MAY LOSE VALUE | NOT A DEPOSIT | NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY